As the second half of 2026 begins, the global economy faces a complex web of interconnected risks, with the fragile peace between the United States and Iran emerging as the central variable. A new briefing from Oxford Economics outlines how the durability of this agreement will determine whether the world benefits from lower energy costs or confronts a second oil shock.

Ryan Sweet, chief global economist at Oxford Economics, described the US-Iran deal as "the key domino that will determine whether other risks are amplified or dampened." The consultancy projects global annualised growth of 3.1% in the second half, up from an estimated 1.6% in the first half, driven largely by cheaper oil boosting household incomes. However, Sweet puts the odds of a lasting peace at "a coin flip."

If the truce holds, Oxford Economics expects Brent crude to average in the low $70s per barrel, easing inflation and financial conditions across emerging markets and tech valuations. If it breaks, the consequences would ripple far beyond oil markets. Recent military exchanges—including a US attack on Iran and Iranian strikes on Bahrain and Kuwait—have tested the ceasefire, though both sides have so far remained at the negotiating table. Oil prices reacted with a 3% rise, pushing Brent above $76 a barrel.

Sweet warned that a breakdown would not only raise oil prices but also pressure AI supply chains in Asia, force central banks to adopt hawkish stances, tighten financial conditions, and potentially influence the US midterms and Israeli elections. "The cascade runs fast," he said.

Oil Price Divergence and Trade Tensions

Not all analysts share Oxford Economics' outlook. Morgan Stanley's mid-year forecast, published in May, sees crude climbing back to roughly $90 a barrel by year-end, a $20 gap that reflects different bets on the peace process. The World Bank is also more cautious, projecting Brent crude at about $94 a barrel and warning that global GDP growth will slow to 2.5% in 2026.

Sweet highlighted the Strait of Hormuz as a key bellwether. The peace deal committed to restoring traffic through the chokepoint within 30 days, making mid-July the first hard deadline. "A sustained return to 75% or more of pre-war traffic by mid-July would increase the odds that the agreement is holding," he said. Another indicator is whether Iran formally invokes the accord's Lebanon clause over Israeli strikes, and whether its response is military or rhetorical.

Trade policy adds another layer of risk. US Section 122 tariffs are set to expire on 24 July, but Washington plans to replace them with Section 301 levies, likely pushing effective tariff rates higher. The European Commission has more than 50 trade-defence investigations open against China, up from 17 a year ago, and plans to unveil a broader economic security strategy by September. These tensions are particularly relevant for the eurozone, which is already under strain as recession risks mount, as noted by the European Stability Mechanism.

AI Boom and Financial Fragility

The AI boom that has powered financial markets this year is also vulnerable. Oxford Economics notes that the US AI industry depends heavily on semiconductors and hardware from Northeast and Southeast Asia—regions most exposed to any disruption in the Strait of Hormuz. The Bank for International Settlements (BIS) has warned that the AI boom increasingly relies on opaque "circular financing" between chipmakers, cloud giants, and AI labs, as well as lightly regulated private credit, where lending to the sector has quadrupled in five years.

Zhang Tao, the BIS's Asia-Pacific chief, cautioned that the sector's reliance on non-bank funding means an AI downturn could trigger a sharper and faster correction than a traditional banking crisis. Sweet modelled a "tech bust" scenario where US technology stocks fall by 25% over a year. Such a shock would cause the US economy to "grind to a halt," spilling over to technology exporters and investor sentiment worldwide, leaving global growth 1.1 percentage points below Oxford Economics' baseline next year.

Central Banks, Elections, and Calendar Risks

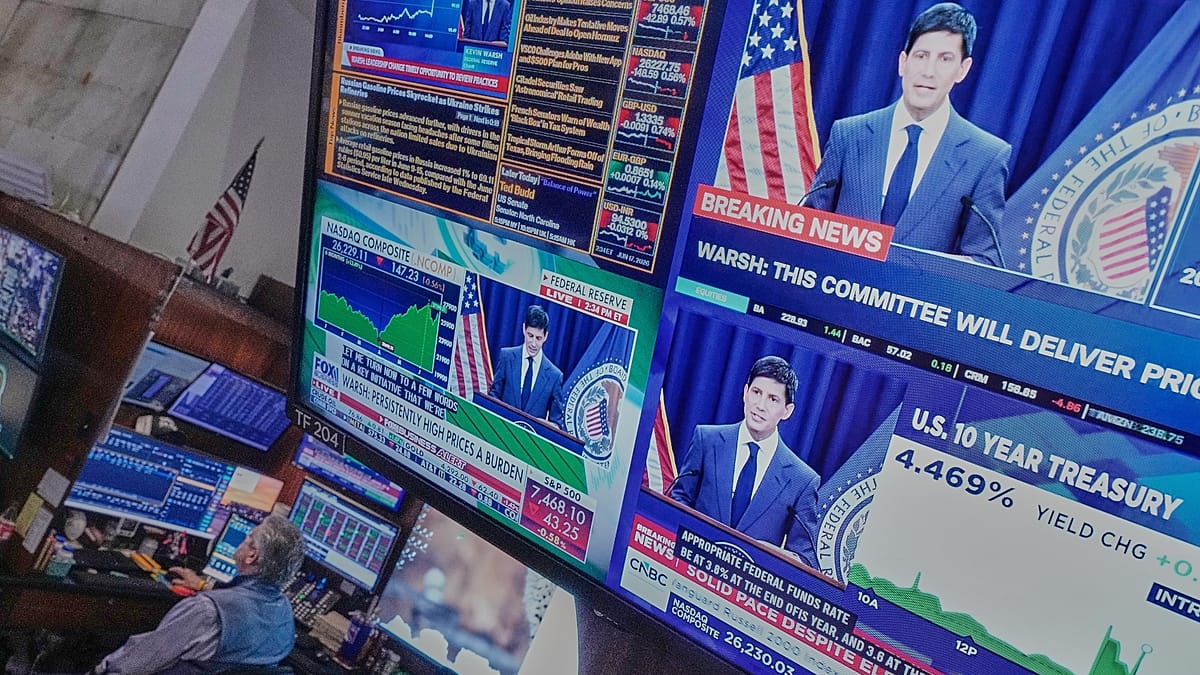

The final dominoes are policy and politics. Oxford Economics expects major central banks to be more dovish than markets anticipate, though they could pivot quickly if Strait of Hormuz traffic falters or AI-input prices signal supply stress. The Federal Reserve's rate decision under chair Kevin Warsh later this month is the nearest test, following June's soft jobs report.

Beyond that, November's US midterms and Israel's general election, due by late October, could influence the Middle East peace process. In September, German state elections may test the coalition behind Berlin's fiscal policy, a key driver of the eurozone economy. Oxford Economics also flags upside risks, from stronger AI-driven productivity to an EU economy that weathered the second quarter surprisingly well.